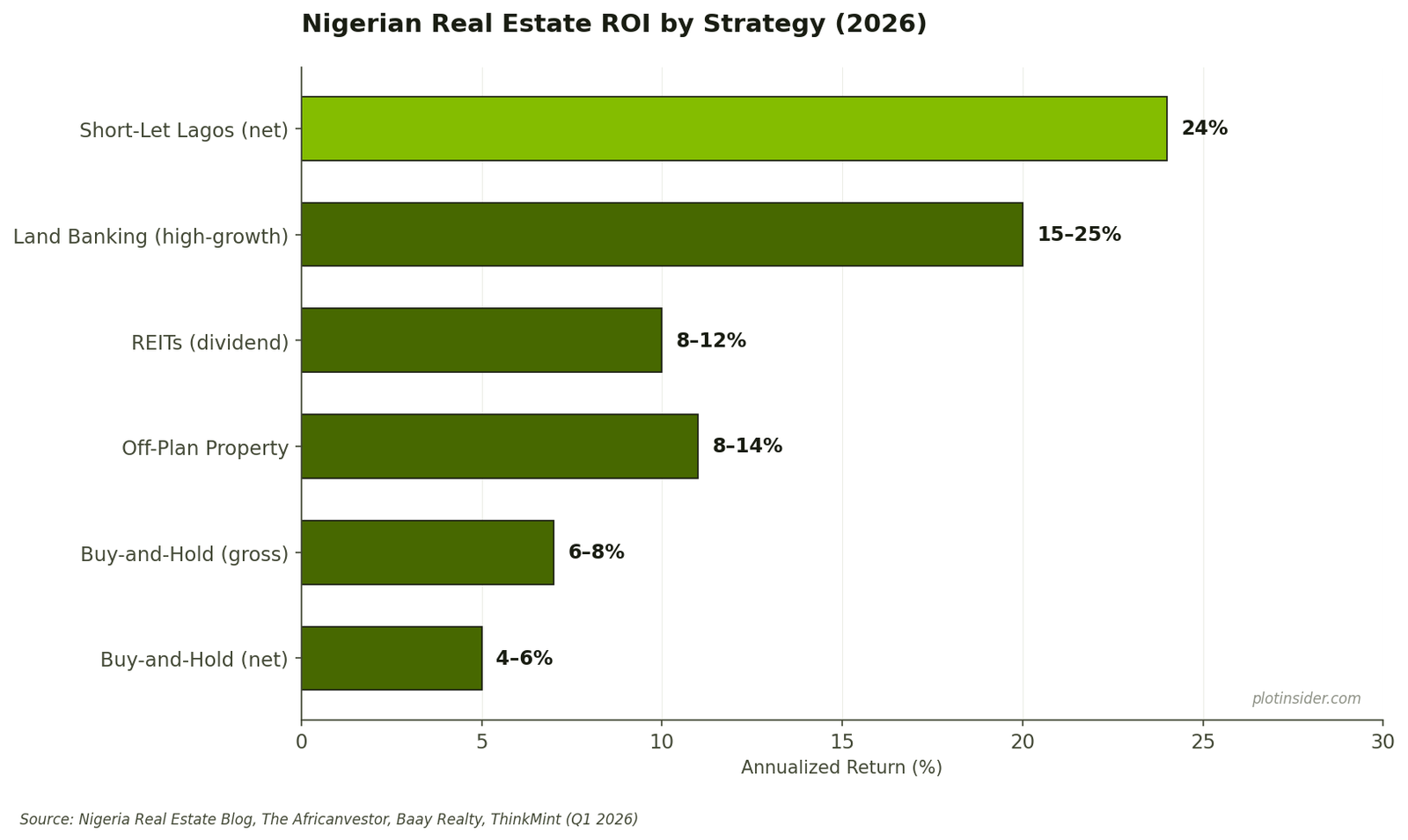

24%. That’s the average net rental yield for short-let apartments in Lagos in Q1 2026, according to Nigeria Real Estate Blog — with prime zones like Lekki Phase 1 delivering 26–32% net after management costs. Compare that to the Nigerian Stock Exchange, where the All-Share Index returned roughly 35% in naira terms in 2024 but has shown dramatic volatility since.

Real estate in Nigeria isn’t one investment — it’s five distinct strategies, each with its own risk profile, capital requirement, and ROI pattern. Pick the wrong one for your situation and you lock up capital in a slow-moving asset. Pick the right one and you beat inflation comfortably, generate hard-currency-adjacent returns, and build a tangible portfolio.

This guide breaks down the five strategies with live 2026 ROI data, capital requirements, and who each strategy actually works for.

Key Takeaways

- Short-let apartments in Lagos averaged 24% net yield in Q1 2026, the highest-returning real estate strategy in Nigeria

- Buy-and-hold rentals in Lagos deliver 6–8% gross yields, with 4–6% net yields after management and tax

- Land banking can double in 3–5 years in high-growth corridors like Ibeju-Lekki and Lagos–Ibadan expressway

- Off-plan apartments offer 40–80% gains over 5 years, roughly 8–14% annualized, per Baay Realty

- Entry capital ranges from ₦1 million (land banking in outer Ogun) to ₦100 million+ (prime Lagos flips)

- Nigerian landlords pay 10% withholding tax on rental income, often deducted at source

What Does It Mean to Invest in Real Estate in Nigeria?

Investing in real estate in Nigeria means deploying capital into land, property, or real estate-backed securities with the goal of generating rental income, capital appreciation, or both. Unlike buying a home to live in, investment property is evaluated primarily by Return on Investment (ROI), rental yield, and capital growth rate.

The five main investment strategies in Nigeria are:

- Buy-and-hold rentals — purchase property, rent it out, collect monthly income

- Short-let operations — furnished Airbnb-style rentals

- Land banking — buying land in growth corridors and holding for appreciation

- Off-plan property — buying under-construction units at a discount

- REITs and property funds — fractional real estate exposure through listed securities

Each strategy has a distinct risk-return profile. The table below compares them at a glance.

Why Nigerian Real Estate Still Delivers in 2026

Three factors make Nigerian real estate a viable investment class despite macroeconomic headwinds.

Inflation hedge. Nigeria’s inflation rate remains above 20%. Naira-denominated property in Lagos has historically appreciated at or above inflation, with 2025 price growth hitting 18% per The Africanvestor.

Rental yield premium. Lagos gross rental yields range from 6–8% in mid-market areas, and up to 24% in short-let operations. This comfortably beats fixed deposits and bonds.

Scarcity of trusted alternatives. With Nigerian equity markets volatile and bank deposits eroded by inflation, many high-net-worth Nigerians are channeling capital into tangible assets. Real estate captures most of that flow.

Strategy 1: Buy-and-Hold Rentals

Capital required: ₦30 million – ₦500 million+ Gross ROI: 6–8% in mid-market Lagos Net ROI: 4–6% after management (10–15%) and withholding tax (10%) Best for: Passive investors seeking steady naira cashflow

How It Works

You buy a residential property — typically a 1- to 3-bedroom apartment — and rent it out on annual contracts. Tenants pay 1–2 years upfront in most Nigerian cities.

The Live 2026 Numbers

According to The Africanvestor’s Lagos rental yields update (February 2026):

| Apartment Type | Typical Gross Yield | Tenant Profile |

|---|---|---|

| Studios | 5–7% | Young singles, expatriates |

| 1-bedroom | 3–4% | Young professionals |

| 2-bedroom | 4–6% | Small families, professionals |

| 3-bedroom | 4–5% | Mid-career families |

2-bedroom apartments deliver the most consistent yield because they hit the sweet spot of broad tenant demand and purchase prices that haven’t inflated as aggressively as larger prime-area units.

Yield by Lagos Neighborhood

| Neighborhood | Gross Yield | Profile |

|---|---|---|

| Yaba | 6–9% | Tech workers, students |

| Ikeja GRA | 5–8% | Airport-adjacent professionals |

| Ogudu GRA / Magodo Phase 2 | 5–8% | Mainland middle-upper class |

| Lekki (inner) — Osapa, Ikate | 5–8% | Tech entrepreneurs |

| Banana Island / Old Ikoyi | Below 5% | Diplomats, ultra-HNW |

Who It Works For

Passive investors with ₦30M+ who want predictable income and don’t mind a 4–6% net yield. Not ideal for investors seeking aggressive capital growth.

Strategy 2: Short-Let / Airbnb Operations

Capital required: ₦25 million – ₦80 million (property) + ₦3–5M (furnishing) Net ROI: 24% average in Lagos Q1 2026, 26–32% in prime zones Best for: Active investors willing to manage operations or hire managers

How It Works

You buy or lease a property, furnish it to hotel-grade standards, and rent it out by the day or week on platforms like Airbnb, Booking.com, or local alternatives. Your tenant turnover is constant, but so is your cashflow.

The Live 2026 Numbers

Nigeria Real Estate Blog’s Q1 2026 analysis found:

- Average Lagos short-let net yield: 24%

- Prime zones (Lekki Phase 1, parts of Ikoyi, VI): 26–32% net

- Occupancy requirement to hit these yields: 60–75%

- Daily rates: ₦40,000–₦150,000 depending on location and specifications

Top-Performing Cities and Zones

| City / Zone | Avg. Daily Rate | Peak Occupancy |

|---|---|---|

| Lekki Phase 1 | ₦50k–₦120k | 70–85% |

| Ikoyi | ₦80k–₦200k | 65–80% |

| Victoria Island | ₦60k–₦150k | 70–80% |

| Abuja (Jabi, Wuse II) | ₦40k–₦90k | 60–70% |

The catch here…

Short-let yields dwarf traditional rentals, but they demand active management. You’ll need reliable power (inverter + generator), professional cleaning, a photographer, dynamic pricing, and either a manager or your own time. Done wrong, short-let yields collapse to below buy-and-hold levels.

Who It Works For

Investors with ₦30M+, appetite for active management, and a location in Lekki, Ikoyi, VI, Lagos Island, or Abuja’s Wuse II / Jabi corridor.

Strategy 3: Land Banking

Capital required: ₦1 million – ₦50 million per plot ROI: Land can double in 3–5 years in high-growth corridors Best for: Patient investors with long time horizons and strong title due diligence

How It Works

You buy land in a corridor expected to appreciate (often because of infrastructure development) and hold until values rise. You collect no cashflow during the hold — appreciation is 100% of the return.

The Live 2026 Numbers

According to The Africanvestor’s Lagos property forecasts:

- Ibeju-Lekki: price growth of 20–25% annually due to Lekki Deep Sea Port and Free Trade Zone

- Osapa London–Ikate–Agungi corridor: 15–20% annual growth

- Yaba: 12–18% annual growth driven by Red Line rail

- Lagos–Ibadan expressway corridor and Epe axis: emerging 10–15% growth zones

Entry Capital Examples

| Corridor | Typical Plot Price | 5-Year Appreciation Target |

|---|---|---|

| Ibeju-Lekki (near Free Zone) | ₦3M – ₦15M | 2x – 3x |

| Epe | ₦1M – ₦5M | 1.5x – 2.5x |

| Ogun (Mowe/Simawa) | ₦800k – ₦3M | 1.5x – 2.5x |

| Abuja outskirts (Lugbe, Karsana) | ₦2M – ₦8M | 1.5x – 2x |

The Risk

Land banking’s biggest risk isn’t price — it’s title. Fake layouts, unverified land, and community disputes still affect Nigerian land markets. Always verify Certificate of Occupancy (C of O), survey plans, and physical possession before payment.

Our guide on how to write a legally sound land agreement in Nigeria covers the clauses and templates that protect you in these transactions.

Who It Works For

Long-horizon investors with at least ₦1M to deploy, the patience to wait 3–5 years, and a commitment to rigorous title due diligence.

Strategy 4: Off-Plan / Pre-Construction Property

Capital required: ₦20 million – ₦100 million+ ROI: 40–80% gain over 5 years (~8–14% annualized), per Baay Realty Best for: Investors who can wait 18–36 months for handover

How It Works

You buy an under-construction unit at discounted pre-launch pricing. When the development completes, units typically sell for 30–50% above your entry price. You then either flip or rent out.

The Live 2026 Numbers

Baay Realty’s Foreshore example: a 2-bedroom apartment bought off-plan at ₦40M can be worth ₦55–65M at handover (2 years), reaching ₦70–90M by year five. That’s a 40–80% gain before any rental income.

By contrast, fully built comparable homes in Lekki Phase 1 or VI start at ₦100M+. Off-plan effectively gives you the same home at 50% of the price — if the developer delivers.

The Risk

Developer execution. Nigerian construction delays are real. According to multiple industry sources, roughly 20–30% of off-plan projects miss their original handover date by 6+ months. Vet the developer’s track record, payment milestones, and escrow arrangements before committing.

Who It Works For

Diaspora Nigerians and high-net-worth locals with ₦20M+ who can tolerate an 18–36 month lock-up period in exchange for entry-price discounts.

Strategy 5: REITs and Property Funds

Capital required: ₦10,000 – ₦10M+ (very flexible) ROI: 8–12% dividend yield + modest capital appreciation Best for: Small-ticket investors seeking liquid real estate exposure

How It Works

Real Estate Investment Trusts (REITs) pool capital from multiple investors to buy and manage income-generating properties. You buy shares in the REIT, receive dividends, and can sell anytime.

Nigeria has three listed REITs: UPDC REIT, Skye Shelter Fund, and Union Homes REIT. All trade on the Nigerian Exchange (NGX).

The Live 2026 Numbers

REIT yields in Nigeria typically range from 8–12% in dividend income, plus modest capital appreciation. Entry is as low as ₦10,000 — the price of one share plus broker fees.

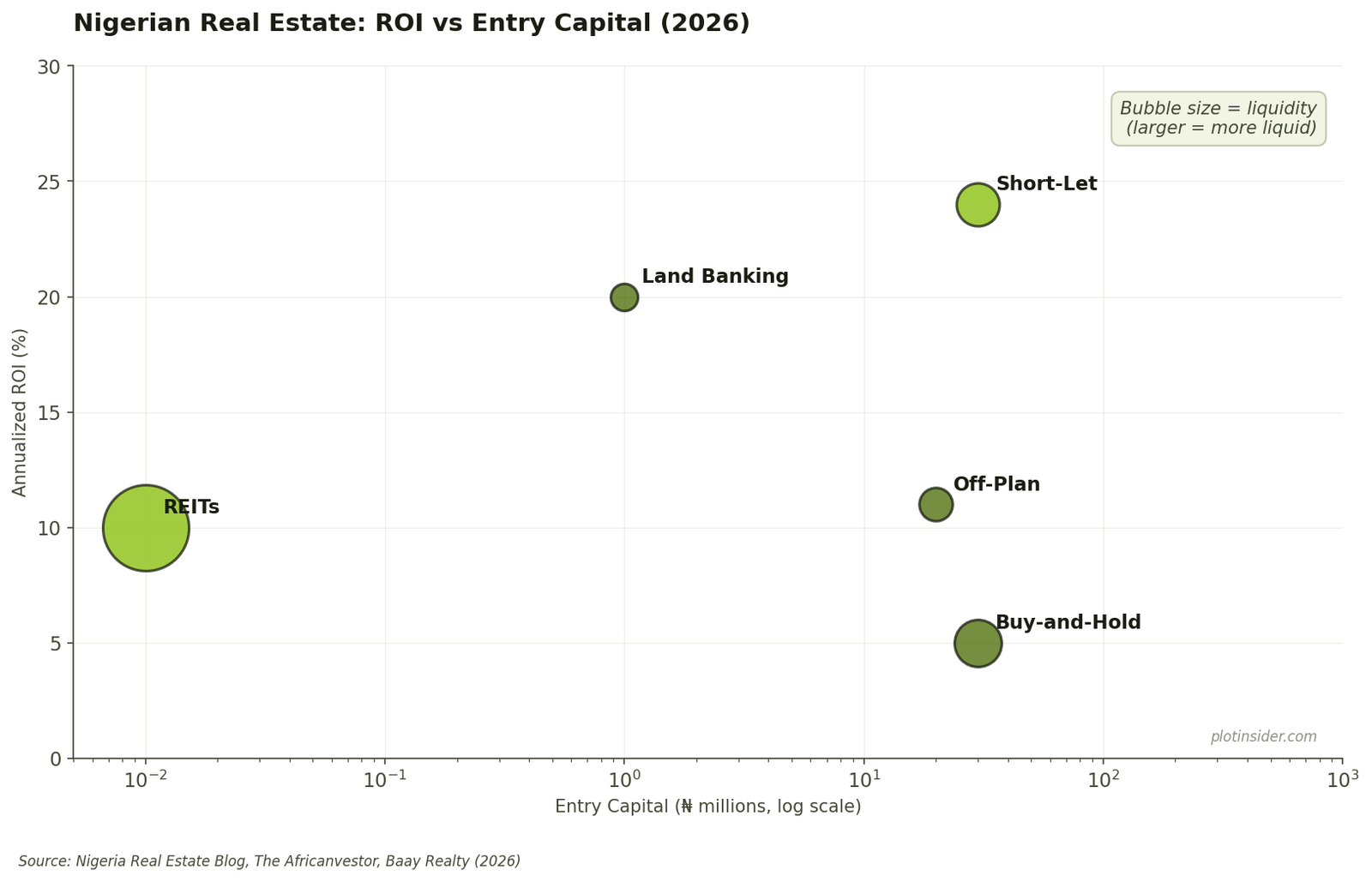

Comparison Table: Five Strategies Side-by-Side

| Strategy | Entry Capital | Annualized ROI | Liquidity | Active Management |

|---|---|---|---|---|

| Buy-and-hold rentals | ₦30M+ | 4–6% net | Low | Medium |

| Short-let | ₦30M+ | 24% (Lagos Q1 2026) | Low | High |

| Land banking | ₦1M+ | 15–25% | Very low | Low |

| Off-plan | ₦20M+ | 8–14% | Very low | Low |

| REITs | ₦10k+ | 8–12% dividend | High | None |

Common Mistakes When Investing in Real Estate in Nigeria

Three mistakes recur across all five strategies.

Skipping title verification. Even in Lagos and Abuja prime areas, fraudulent deeds circulate. Always verify C of O or Governor’s Consent directly at the relevant State Lands Bureau before payment.

Underestimating net yields. Gross rental yields look attractive until you subtract 10% withholding tax, 10–15% property management fees, service charges, and vacancy costs. Budget conservatively: Lagos net yields typically run 1.5–2.5% below gross.

Ignoring flood and infrastructure risk. Flood-prone parts of Lagos and Port Harcourt trade at significant discounts for good reason. Similarly, land in corridors without functional roads stagnates even when nearby areas appreciate.

For first-time investors, our guide on the 4 types of real estate and which builds wealth fastest covers the asset-class fundamentals you need before choosing a strategy.

Conclusion: Match the Strategy to Your Capital and Time Horizon

Nigerian real estate in 2026 offers five genuinely different investment strategies. The right one for you depends on three questions: how much capital can you deploy, how long can you wait, and how involved do you want to be?

If you have ₦10k–₦1M and want liquidity: REITs. If you have ₦1M–₦10M and can wait 5 years: land banking. If you have ₦20M–₦60M and can wait 2–3 years: off-plan. If you have ₦30M+ and want passive income: buy-and-hold. If you have ₦30M+ and can manage actively: short-lets — the clear yield winner at 24% net in Q1 2026.

At Plot Insider, we track Nigerian real estate returns every quarter — yields, transaction data, growth corridors, and developer performance. Bookmark us for the data-driven view of where your investment capital actually works hardest.

Frequently Asked Questions

What is the best real estate investment strategy in Nigeria in 2026?

Short-let operations deliver the highest returns in Nigeria in 2026, averaging 24% net yield in Lagos during Q1 2026, with prime zones like Lekki Phase 1 hitting 26–32% net. However, short-lets require active management. For passive investors, land banking in growth corridors like Ibeju-Lekki (20–25% annual appreciation) offers higher returns than traditional rentals.

How much do I need to start investing in real estate in Nigeria?

You can start investing in Nigerian real estate with as little as ₦10,000 through REITs listed on the Nigerian Exchange. Land banking in emerging Ogun State corridors starts from ₦1 million per plot. Traditional buy-and-hold rentals require ₦30 million+ for a Lagos 2-bedroom apartment. Off-plan entry typically starts at ₦20 million.

What rental yield should I expect in Lagos in 2026?

Lagos gross rental yields range from 6–8% in mid-market areas, according to The Africanvestor’s 2026 analysis. Net yields after management fees (10–15%) and 10% withholding tax typically land between 4–6%. Short-let apartments in Lagos averaged 24% net yield in Q1 2026 — a dramatically higher return but requiring active management.

Is land banking still profitable in Nigeria?

Yes. Land in high-growth Nigerian corridors can double in 3–5 years, according to Baay Realty’s 2026 analysis. Ibeju-Lekki leads at 20–25% annual appreciation, driven by the Lekki Deep Sea Port and Free Trade Zone. The key risks are title verification, flooding, and the long holding period with no cashflow.

Sources

- Real Estate Investment Strategies in 2026 — Baay Realty. https://baayrealty.com/real-estate-investment-strategies-in-2026-nigeria/

- Lagos Latest Rental Yields Data (2026) — The Africanvestor. https://theafricanvestor.com/blogs/news/lagos-nigeria-rental-yields

- Top 10 Places in Nigeria to Invest in Rental Property in 2026 — ThinkMint. https://www.thinkmint.ng/buyrealestate/top-10-places-in-nigeria-to-invest-in-rental-property-in-2026/

- Nigeria Real Estate Price Forecast 2026 — ThinkMint. https://www.thinkmint.ng/buyrealestate/nigeria-real-estate-price-forecast-2026-what-investors-should-know/