14.925 million.

That’s the official housing deficit figure released in January 2026 by the National Housing Data Technical Committee, a multi-agency body coordinated by the Nigeria Mortgage Refinance Company (NMRC) under the Federal Ministry of Housing and Urban Development.

But ask any developer, real estate consultant, or housing NGO, and they’ll give you a number almost twice as large: 22 to 28 million units, a figure cited by the Federal Mortgage Bank of Nigeria, the Central Bank of Nigeria, and widely referenced by BusinessDay, Punch, and international analysts.

Which number is right? Both — and understanding the gap between them is the key to understanding Nigeria’s housing crisis.

Key Takeaways

- Nigeria’s government officially pegs the housing deficit at 14.925 million units (January 2026, NMRC data). Industry estimates range from 22 to 28 million. Both figures are correct — they measure different things.

- An additional 15.2 million existing homes are classified as structurally inadequate or substandard, meaning the total housing crisis affects approximately 30 million households.

- Closing the gap would cost between ₦21 trillion and ₦59 trillion ($15–$40 billion USD), yet Nigeria builds fewer than 100,000 units per year — against a need of 550,000–700,000 annually.

- Lagos accounts for the largest share of the deficit, having delivered only 9,970 housing units in six years despite a city population exceeding 21 million.

- Mortgage penetration remains below 1% of GDP. Only 32.5% of urban Nigerians own their homes. The housing crisis is fundamentally a financing crisis.

Why the Numbers Don’t Match: Quantitative vs Qualitative Deficit

The 14.925 million figure measures the quantitative deficit — the raw number of additional housing units needed to give every Nigerian household a physical dwelling. It was derived through a more scientific methodology than previous estimates, according to NMRC chairman Dr. Taofeek Olatinwo.

The 22–28 million figure includes both the quantitative deficit AND the qualitative deficit — homes that exist but fail to meet the United Nations’ minimum standards for habitability. According to Punch newspaper’s analysis of the same government data, an additional 15.2 million existing homes are classified as structurally inadequate or outright substandard.

Combined: approximately 30 million Nigerian households either have no home at all or live in a home that doesn’t meet basic safety and livability standards.

| Metric | Figure | Source |

|---|---|---|

| Quantitative deficit (units needed) | 14.925 million | NMRC / Federal Ministry, Jan 2026 |

| Qualitative deficit (substandard homes) | 15.2 million | Federal Ministry Technical Committee |

| Combined housing crisis | ~30 million households | Calculated from above |

| Industry-cited total deficit | 22–28 million | FMBN, CBN, industry estimates |

| Cost to bridge the gap | ₦21T – ₦59T ($15B–$40B) | Multiple sources |

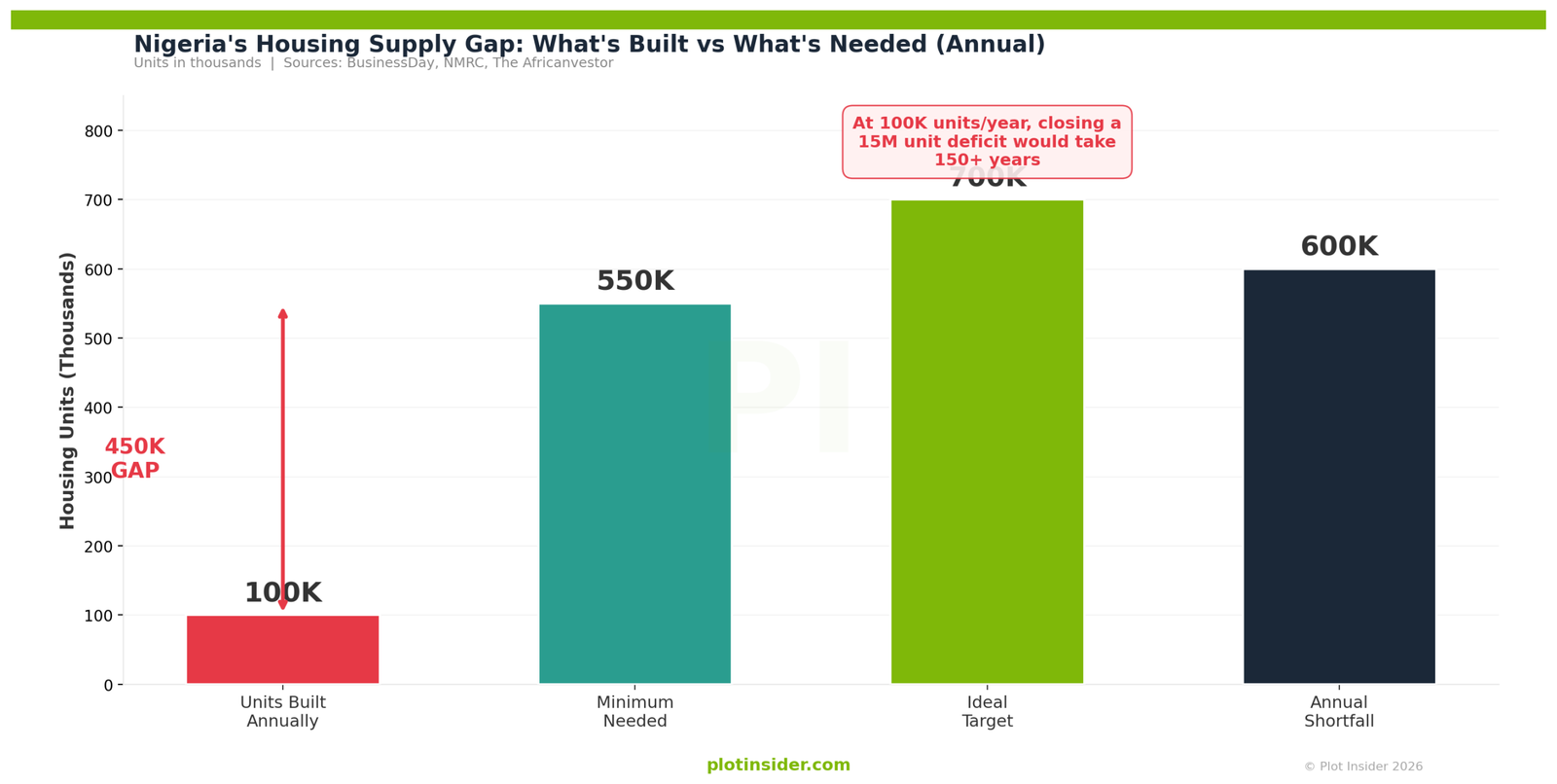

Nigeria Builds 100,000 Units Per Year. It Needs 700,000.

The supply-demand mismatch is staggering. According to BusinessDay’s analysis, Nigeria delivers fewer than 100,000 new housing units annually. The estimated requirement to begin closing the deficit is 550,000 to 700,000 units per year over the next decade, according to Nigeria Housing Market.

At the current construction rate, it would take over 150 years to close a 15 million unit deficit — and the deficit grows each year because Nigeria’s population expands by approximately 2.5% annually. The housing gap is widening, not narrowing.

Here’s how the math breaks down:

| Factor | Data Point |

|---|---|

| Current annual housing delivery | ~100,000 units |

| Annual units needed | 550,000–700,000 |

| Annual delivery gap | 450,000–600,000 units |

| Population growth rate | 2.5% per year (~5.5 million people) |

| Urbanization rate | 4.1% annually |

| Current urban population | Over 60% (130+ million) |

| Projected population by 2050 | 400 million (UN estimate) |

Sources: BusinessDay, The Africanvestor, Nigeria Housing Market

Where the Deficit Is Worst: City-Level Data

The housing deficit is not evenly distributed. Over 60% of new residential developments are concentrated in three cities — Lagos, Abuja, and Port Harcourt — according to The Africanvestor. Yet even in these cities, supply falls catastrophically short.

Lagos: The Epicenter

Lagos accounts for the single largest share of Nigeria’s housing deficit. The Lagos State Government itself acknowledges the crisis, having delivered only 9,970 home units over six years — in a city of 21+ million people where housing demand grows by an estimated 4.3% annually.

A one-bedroom apartment in Lagos now rents for over ₦1 million annually, according to BusinessDay — nearly double the national minimum wage of ₦70,000 per month (₦840,000 per year). For millions of Lagos residents, rent alone consumes more than 100% of their income.

Abuja: Supply Meets Less Than 10% of Demand

In 2024, Abuja built over 5,000 new housing units — but this met less than 10% of the city’s annual housing demand. The FCT’s structured planning system creates higher-quality housing stock, but at prices inaccessible to most civil servants and middle-income workers.

Secondary Cities: Growing Demand, Almost Zero Supply

Cities like Ibadan, Kano, Enugu, and Benin City are absorbing hundreds of thousands of new residents annually through rural-urban migration. But formal housing construction in these cities is negligible. Most new shelter takes the form of informal self-build construction — often without planning approval, engineering oversight, or title documentation.

Why the Deficit Keeps Growing: 5 Structural Failures

The housing deficit isn’t just a construction problem. It’s a system failure across five interconnected areas.

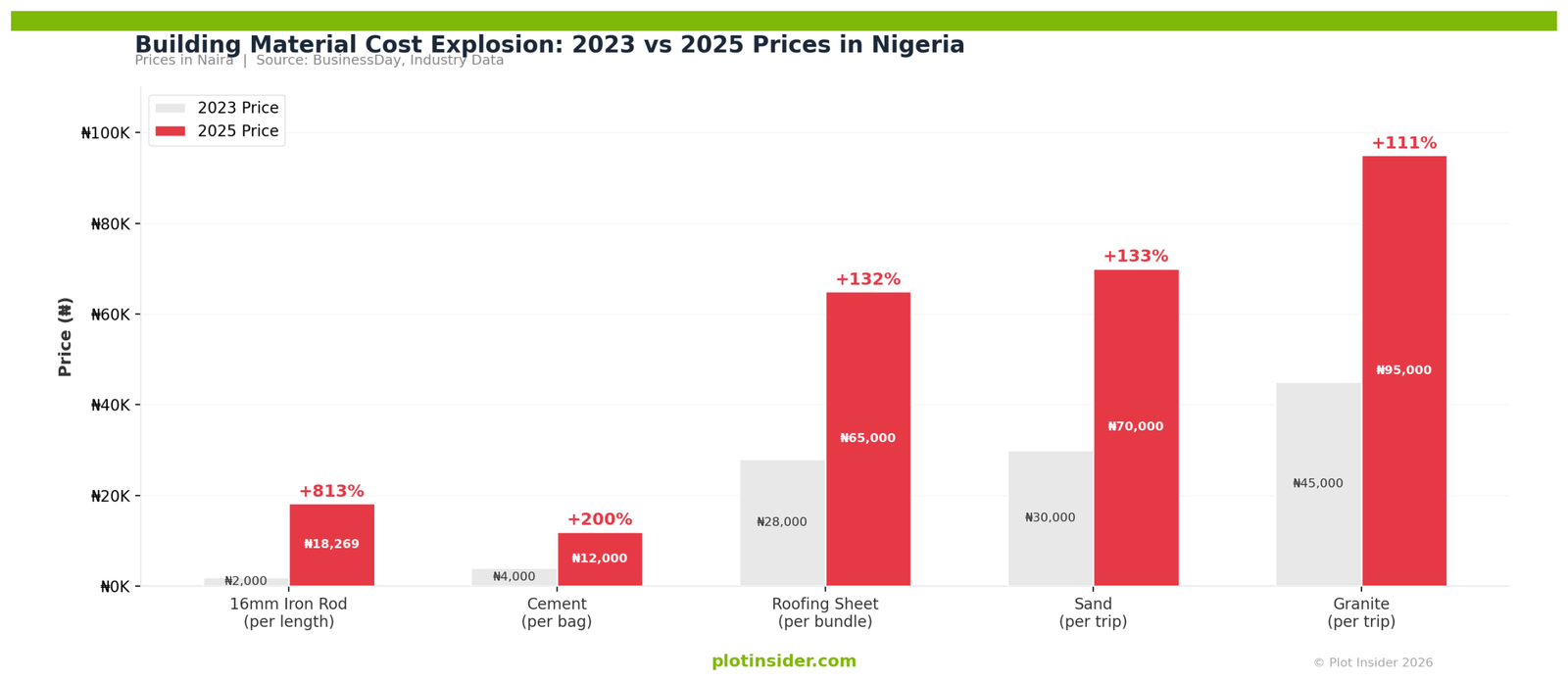

1. Construction Costs Have Exploded

Building a home in Nigeria has become dramatically more expensive due to naira devaluation and import dependency. According to BusinessDay:

| Material | 2023 Price | 2025 Price | % Increase |

|---|---|---|---|

| 16mm iron rod | ₦2,000 | ₦18,269 | +813% |

| Cement (per bag) | ₦4,000 | ₦10,200–₦12,000 | +155%–200% |

These are not gradual increases — they’re supply shocks driven by foreign exchange instability, since many building materials are imported or require imported inputs. When the naira loses value, construction costs rise immediately.

2. Mortgage Finance Is Virtually Non-Existent

Mortgage penetration in Nigeria stands below 1% of GDP, compared to over 50% in developed markets like the US and UK. Interest rates on available mortgages range from 15% to 25% annually.

This means the overwhelming majority of Nigerian homebuyers must pay cash — which only approximately 5% of the population can afford for a full home purchase, according to Federal Mortgage Bank data cited by BusinessDay. The people who need housing most are the people who can least afford it.

3. Land Access and Title Bureaucracy

The Land Use Act of 1978 vests all land in state governors, creating a bottleneck for every land transaction. The process of obtaining a Certificate of Occupancy or Governor’s Consent can take 6–24 months and cost 10%–15% of the property value in fees.

According to BusinessDay, complicated titling processes, opaque land registries, and high acquisition fees significantly slow down development in states like Lagos and Abuja. An estimated $300 billion in land assets sits as “dead capital” because owners lack formal title documentation.

4. Urbanization Outpaces Everything

Nigeria’s urban population is growing at 4.1% annually — one of the fastest rates in the world. By 2050, the population is projected to exceed 400 million, according to United Nations data cited by Businessday. More than 60% will live in cities.

Every year, millions of Nigerians migrate from rural areas to Lagos, Abuja, Port Harcourt, Ibadan, and Kano seeking economic opportunity. They need housing immediately — but the formal supply pipeline can’t keep up.

5. Government Housing Programs Underdeliver

The Renewed Hope Housing Scheme aims to deliver 300,000 homes nationally, according to Octo5 Holdings. Even if fully delivered — which is historically unlikely — this would cover less than half of one year’s annual requirement (550,000–700,000 units).

Lagos State, Nigeria’s most resourced state government, delivered 9,970 units over six years. At that rate, it would take Lagos alone over 600 years to close its share of the national deficit.

The Affordability Crisis: Who Can Actually Buy a Home?

Only 32.5% of urban Nigerians own their homes, according to Nigeria Housing Market. The remaining 49%+ rely on rented accommodation, and a significant portion lives in informal or shared housing.

Here’s the affordability math for a typical Nigerian:

| Factor | Data |

|---|---|

| National minimum wage | ₦70,000/month (₦840,000/year) |

| Average 2-bed apartment (national) | ₦28.5 million purchase price |

| Years of minimum wage to buy (no expenses) | 34 years |

| Average Lagos 2-bed apartment | ₦70 million purchase price |

| Years of minimum wage to buy in Lagos | 83 years |

| Average Lagos 1-bed annual rent | ₦1 million+ |

| Rent as % of minimum wage | 119% |

The data is clear: homeownership through income alone is mathematically impossible for the majority of Nigerians. Without fundamental changes to mortgage access, construction costs, and land policy, the deficit will continue growing.

What Would It Take to Close the Gap?

Bridging Nigeria’s housing deficit requires intervention across four areas simultaneously.

Scale affordable housing construction. Nigeria needs to move from 100,000 units per year to at least 550,000. This requires industrial-scale approaches: prefabricated housing, alternative building materials (compressed earth blocks, bamboo framing), and streamlined planning approvals.

Fix mortgage finance. Mortgage rates must come down from 15%–25% to single digits for homeownership to be viable for middle-income earners. The Central Bank’s introduction of single-digit NHF mortgage rates is a step — but access remains extremely limited.

Reform land administration. Digitizing land registries, reducing C of O processing times, and lowering transaction costs would unlock billions in “dead capital” and accelerate development. Lagos and Abuja have made progress; most states have not.

Invest in secondary cities. Concentrating 60% of housing development in three cities isn’t sustainable. Secondary cities like Ibadan, Asaba, Uyo, and Abeokuta need infrastructure investment that makes them viable alternatives to Lagos and Abuja.

What the Deficit Means for Real Estate Investors

For investors, the housing deficit isn’t just a social problem — it’s the fundamental driver of Nigeria’s property market dynamics.

A 15-million-unit shortage means demand will structurally outpace supply for decades. This supports sustained price appreciation, strong rental yields (6%–9% in emerging areas), and consistent tenant demand. As long as the deficit exists, well-located property in Nigerian cities will hold and grow value.

However, the deficit also creates risks. Persistent unaffordability limits the buyer pool, concentrates wealth in property-owning minorities, and creates political pressure for rent regulation or forced price controls — all of which could disrupt investment returns.

Smart investors are positioning in the gap between what the market needs and what it currently delivers: affordable to mid-market housing in infrastructure-driven corridors where demand is highest and supply is weakest.

Conclusion

Nigeria doesn’t have a housing deficit — it has a housing emergency. Whether you use the government’s 14.9 million figure or the industry’s 28 million, the conclusion is the same: the country builds a fraction of what it needs, costs are rising faster than incomes, and the gap widens every year.

The data presented in this report shows a crisis measured in trillions of naira, affecting tens of millions of households, with no short-term solution in sight. Understanding these numbers isn’t just academic — it’s the foundation for every investment decision, policy proposal, and development strategy in Nigerian real estate.

Plot Insider publishes this kind of data-driven analysis because we believe the housing crisis demands evidence, not guesswork. Explore more intelligence on Nigeria’s property market on our homepage, and read our state-by-state land price index to see how prices compare across the country.

FAQs

What is Nigeria’s housing deficit in 2026?

The National Housing Data Technical Committee officially pegs Nigeria’s quantitative housing deficit at 14.925 million units as of January 2026. However, when including the 15.2 million existing homes classified as structurally inadequate, the total housing crisis affects approximately 30 million households. Industry estimates that combine both measures range from 22 to 28 million units.

How many houses does Nigeria need to build per year?

Nigeria needs to build 550,000 to 700,000 housing units annually over the next decade to begin closing the deficit, according to multiple industry analyses. The country currently builds fewer than 100,000 units per year — an annual shortfall of at least 450,000 units.

Why is housing so expensive in Nigeria?

Three factors drive housing costs: construction material inflation (iron rods up 813% since 2023, cement up 155%–200%), foreign exchange instability that increases import costs, and land scarcity in urban areas compounded by bureaucratic title processes. These factors have pushed even basic homeownership beyond the reach of most Nigerian wage earners.

Can the housing deficit be solved?

The deficit can be reduced but not eliminated quickly. It would require simultaneously scaling construction to 550,000+ units per year, reducing mortgage rates to single digits, digitizing land registries, and investing in secondary cities. At the current pace of delivery (~100,000 units/year), closing a 15 million unit gap would take over 150 years.

Sources

- Federal Ministry of Information and National Orientation — National Housing Data Technical Committee Releases New Data, January 2026

- BusinessDay — Priced Out: The Harsh Economics Behind Nigeria’s Housing Crisis, 2025

- Punch — Revisiting Nigeria’s Housing Deficit, 2026

- The Africanvestor — Nigeria Real Estate Market Statistics, 2026

- Nigeria Housing Market — Rent Hikes and Housing Crisis, 2026